The Big Freeze: Gas Storage Scenario Update 12.12.22

Coming off a historically warm November, we have been hit by a frigid start to December. Low temperatures have begun emptying stockpiles faster than anticipated.

If you enjoy my content, please consider supporting my work here and on Twitter with a premium Substack subscription. I will be launching a Substack chat for premium subscribers this week, where you can ask me questions, chat and I will post regular small updates on events of interest.

Firstly, I apologize for my my absence the last two weeks. I have had a very busy schedule that did not allow me time to update my models. Last weekend I was invited to speak at Stratcom Summit 2022 in Istanbul, where I spoke about the rapid growth of the OSINT community, as well as some of the pitfalls and growing pains the community is currently faced with. Luckily, this two week absence has given me more data for the cold start to December, which has allowed me to make an additional parameter for this week.

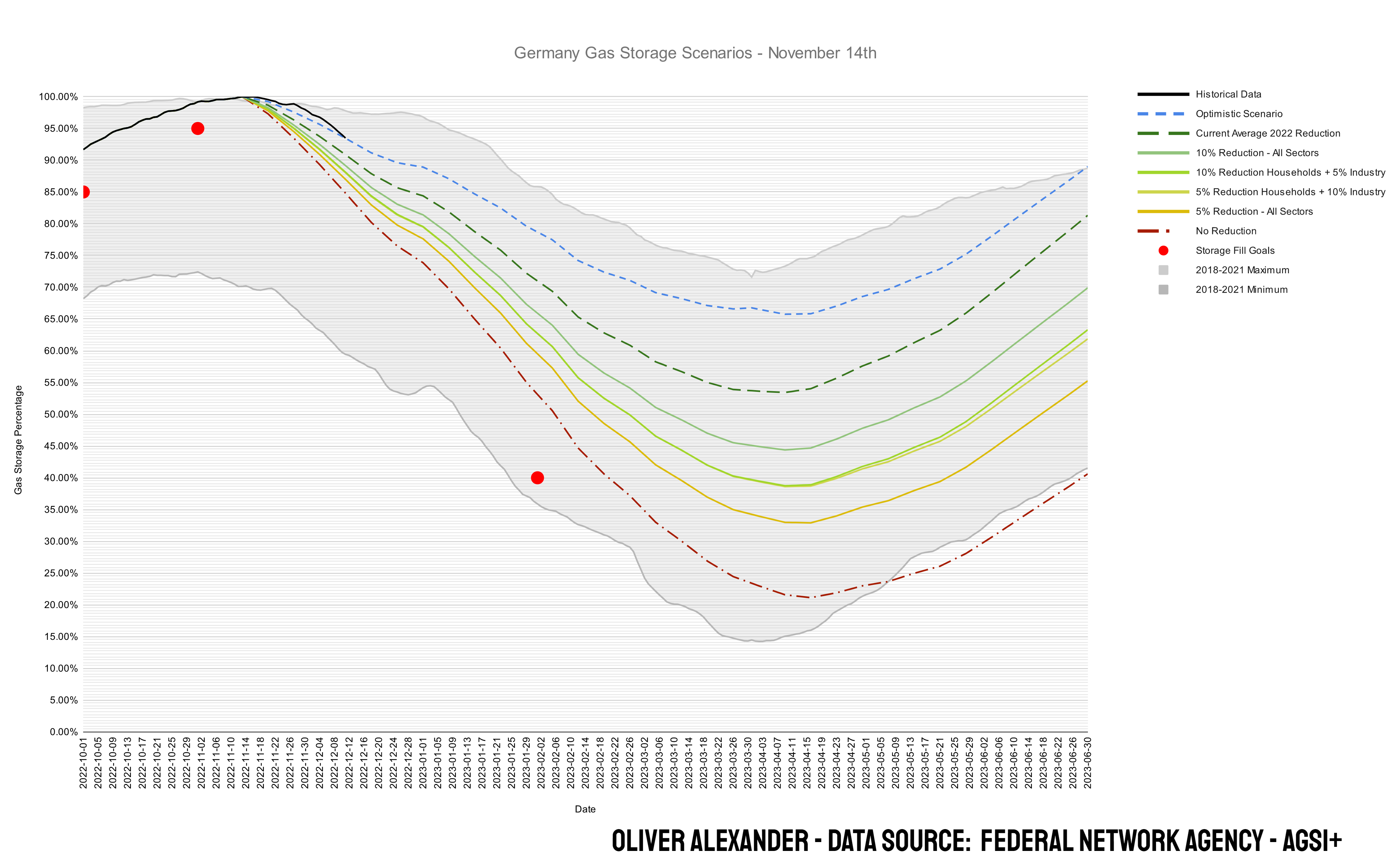

The first two weeks of December have been colder than average, a rapid change from the the previous two months of temperatures well above the norm. This means that the withdrawals from gas storage facilities is well underway, in order to keep up with the increased demand. Currently, as of Sunday 11th December, German gas storage facilities were filled at 93.5% of their working gas volume. The colder than average weather has meant that savings compared to the norm have diminished, resulting in a quicker drop in gas storage levels than would be optimal. The warm final weeks of November allowed more gas than expected to be saved though, which has helped even out the increased usage so far in December. This can be seen on my 14th November model below, updated to include the historical values up until 11th December.

As you can see from the above graph, gas storage is currently still in line with the “Optimistic Scenario” despite the cold start to December. I expect it to drop below during the next week, as slightly colder than average temperatures continue to be forecast for Germany and Europe. Luckily the longer term climate models still forecast a warmer January, which will hopefully balance out usage again.

For this week’s update to the model, I have slightly lowered expected gas imports for the rest of the year to adjust for the currently lowered imports.

As the gas storage fill level still in line with the “Optimistic Scenario” from the 14th November update, forecast gas levels are continuing to look better than they did a month ago. Had Germany continued to use its normal average gas consumption over the winter without any reductions from the 14th November, gas levels would currently have been at 85% instead of 93.5%. This means that the worst case scenario of “no reduction in gas usage” has gone from a bottom of 23.5% in mid April to 29% in mid April. The continued filling of stores due to warmer than average weather during November have allowed for even this scenario to remain within the 2018-2021 minimum fill levels. As with earlier scenario updates, we continue to see a situation where it is hard to imagine a scenario where Germany runs out of gas this winter without a serious reduction in imports, presumably through the sabotage of gas infrastructure. The chance of Germany running out of gas is currently close to 0%.

All other scenarios with some gas usage reductions mange to keep Germany at a satisfactory level throughout the winter.

The “Optimistic scenario” has attempted adjust for the temperature related gas savings. With this adjustment, German households and businesses have saved around 22% gas compared to the 4 year average. At the same time German industry, which is less affected by weather and has a more stable gas consumption, has saved around 18%. For the optimistic scenario I have accounted for this, with a decrease in savings to 10% for households and 5% for industry from the beginning of April as the winter and immediate danger passes.

Barring any major crisis (import issues, sabotage, unusually cold weather) I continue to estimate that we will see a scenario between the blue and green dashed lines on the scenario graph. The Wilhelmshaven LNG terminal still looks to be on track to become operational around the end of this month, allowing for German LNG supplies to be further strengthened. I will attempt to factor this in properly once we have a solid timeline on when the facility becomes operational. The current cold weather will probably result in a scenario closer to the green dashed line than the optimistic scenario, which still Germany in a decent situation preparing for the 2023 winter.

As we have seen, temperature fluctuations can have a massive impact on the gas usage and level of gas withdrawal from storage. To illustrate this I created a graph below that shows the difference in the “Optimistic Scenario” based on colder than average temperatures. With the slightly below average forecast for next week, I would expect that we will see a drop closer to the red line than the blue line in the near future. The hope is that this will be averaged out in January by a warmer than average month.

Additional information on my scenarios can be read here

Thank you.