Germany Gas Storage Scenarios

Updated location for all future German Gas Storage Scenario models

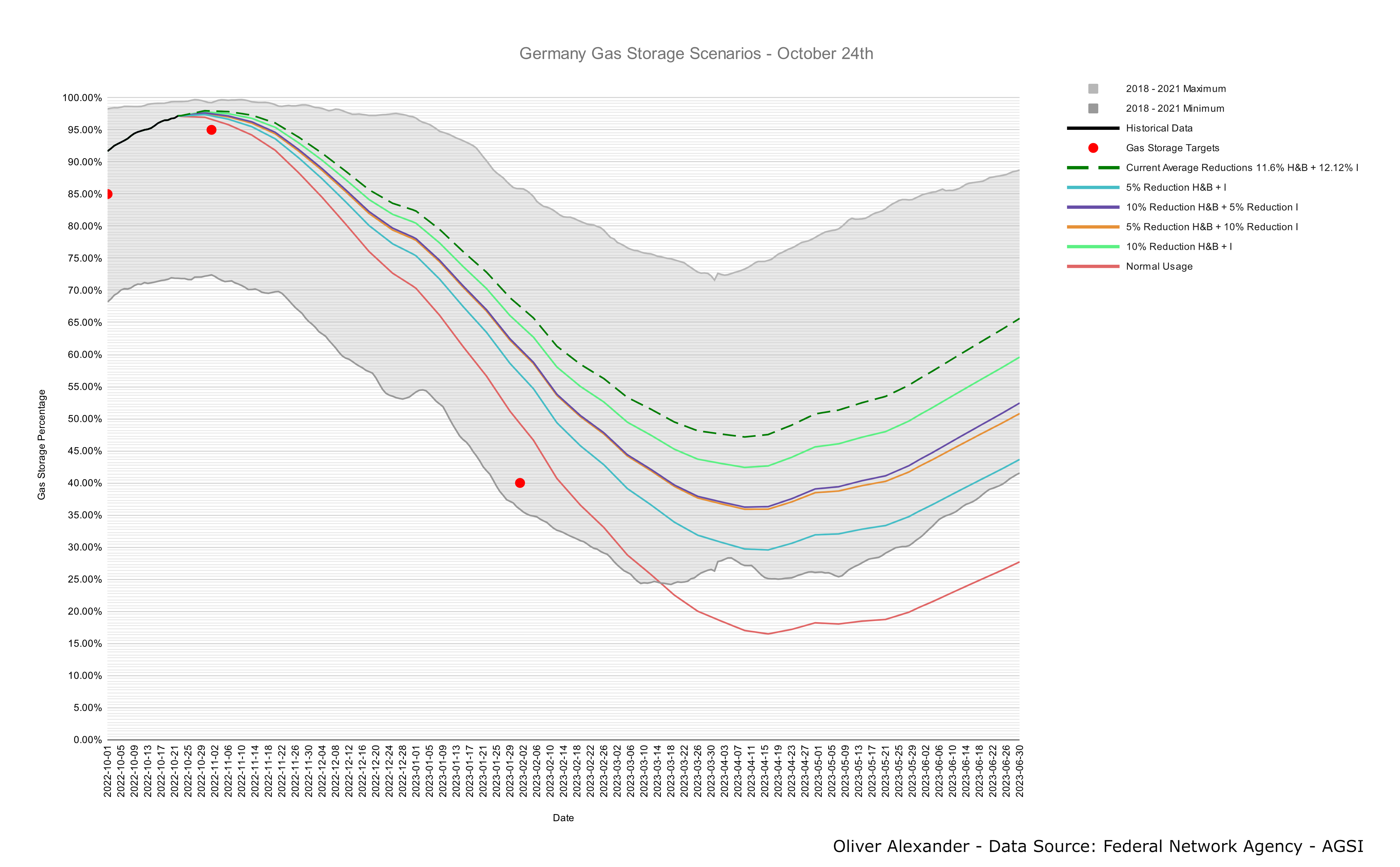

This post will be where I will post updated versions of my German gas storage scenarios. This post will be continuously updated. I have chosen to do it in this way, instead of a new post each time in order to reduce clutter and keep all versions of the model archived in one location. This also means that subscribers who are not interested in the gas situation do not get bombarded with weekly email about my scenarios.

Note: These are continuously updated scenarios and due to the general volatility of the situation the scenarios are hard to predict and the situation may suddenly change rapidly. These scenarios are an estimate based on historical data and assumptions of the situation in the near term future.

Current Version - 24th October 2022

There are two changes in the scenarios for this week’s update that adjust the scenarios slightly, one minor and one major. The minor change is a small down adjustment to German domestic gas production to fall more accurately in line with production at this time.

The major adjustment is a 15-20% increase in German natural gas exports to other countries. In recent days Germany’s natural gas exports have increased marginally, bringing them closer to where there were prior to the complete Nord Stream shut off.

Original Version - 1st October 2022

This is the original version of the scenarios with the addition of new historical data. Historical data on the original will be continuously updated as new versions get released to compare the original to the actual events.

Past Updates:

Past versions of scenarios and reasoning for changes will be moved here with updated known values to compare accuracy:

16th October 2022

This is the first update to the German gas storage scenarios. Newly released German gas import data has made me increase my estimates for Germany’s gas imports over the winter by 5-10%. Through increases from other sources, the total daily gas import is now equivalent to the period where Nord Stream 1 still provided 20% of its capacity to Germany. This increase has shifted all the scenarios above the February 1st goal of 40% storage remaining.

The average reduction in gas usage so far this year among both household and business (SLP) and industrial customers has been adjusted slightly downwards.

So if we have a normal winter (which is mostly warmer than average of the last decades)

nothing terrible would happen. No gas shortage ?